Adidas AG’s leadership and management styles are central to its position as a global leader in sportswear, navigating competitive markets and evolving consumer demands. This section critically evaluates these styles using Transformational Leadership and Situational Leadership models, analysing the leadership structure, key figures such as former CEO Kasper Rorsted and current CEO Bjørn Gulden, and their approaches to managing the organization. Drawing on independent research from Adidas’ investor reports and academic literature, it assesses strengths like innovation and adaptability, alongside weaknesses such as potential resistance to change and coordination challenges, supported by robust evidence. For students exploring similar topics, Leadership Assignment Help can offer valuable guidance in understanding and applying these theoretical models to real-world cases.

Need This? Order Here

Leadership Styles and Academic Models

Adidas’ leadership under Bjørn Gulden, who succeeded Kasper Rorsted in January 2023, exemplifies transformational leadership. This model, defined by idealized influence, inspirational motivation, intellectual stimulation, and individualized consideration, drives organizational change through vision and employee empowerment (Alblooshi, Shamsuzzaman and Haridy, 2020). Gulden’s unconventional move to share his phone number with all employees reflects inspirational motivation, fostering a culture of accessibility and trust (Parekh, 2024). The 2022 Annual Report highlights the "People Leader Experience" program, which trains managers to inspire diverse teams, aligning with intellectual stimulation by encouraging creative problem-solving (ADIDAS AG, 2023a). This approach has revitalized Adidas post-2022, a year marked by financial setbacks under Rorsted’s tenure.

Conversely, situational leadership, which adjusts styles based on follower readiness (Hersey and Blanchard, 1977), is evident in Adidas’ historical and current leadership transitions. Rorsted, CEO from 2016 to 2022, adopted a directive style, emphasizing cost-cutting and digital transformation to address declining profitability (Radaković, TurÄinović and Pejanović, 2023). His goal-oriented management, including, for example, the goal to decrease operating costs by 10% in 2018, was appropriate for an organisation’s workforce during the turnarounds. The change in leadership style from Gulden to a more participative style and focusing on employee involvement as well as brand activation seems to be more appropriate for a recovery stage of the organisation. This is very important especially in the rapidly evolving environment of the apparel business but it has to be balance to ensure that existing structures are not affected.

A deeper look into the two models show how these models are related. The transformational leadership under Gulden focused more on the vision than on the operational aspect, whereas the situational directive leadership by Rorsted might have limited creativity where there was stability. Based on the literature, this pacing increase resilience as leaders have to shift between the two based on the external environment (Verma and Mehta, 2022). Adidas has undergone an organizational transition from Rorsted’s focus on efficiency to Gulden’s focus on people despite some challenges.

Figure 1 Transformational Leadership Model Applied to Adidas

Source: (ADIDAS AG, 2023a)

Leadership Structure and Key Leaders

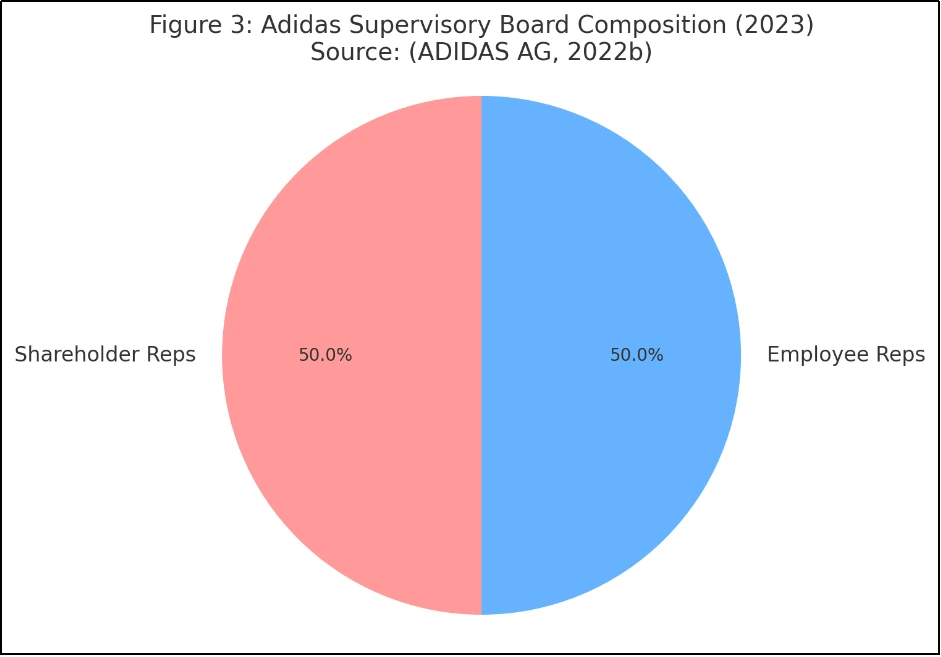

Adidas has a two-tiered board structure that stems from the German corporate laws that requires the company’s Executive Board and the supervisory board. The Executive Board, led by Gulden, includes CFO Harm Ohlmeyer, COO Arthur Hoeld, and CHRO Andrea Holt (who succeeded Amanda Rajkumar in 2024) (ADIDAS AG, 2022a). This team executes strategy, while the Supervisory Board, with 16 members split evenly between shareholder and employee representatives, provides oversight and appoints executives (ADIDAS AG, 2022b). This structure ensures accountability and diverse input, aligning management with shareholder and workforce interests.

Gulden’s leadership contrasts sharply with Rorsted’s. While Rorsted mainly concerned himself on financial rebalancing which he achieved by increasing operating margin to 16% in 2020, Gulden prioritizes cultural transformation to ‘recharge and repair’ the company after making a €512 million net loss in 2022 (ADIDAS AG, 2023b). Ohlmeyer, who is fiscally minded, has been managing the finances of the company prudently and leaves the visionary role to Gulden. Hoeld assumes the method of directive style of leadership to facilitate efficiency in the operations of Adidas where it requires correction in their global supply chain while on the other hand Holt is more of democratic style of leadership where he encourages subordinates to embrace the change and bring out ideas to the table for instance change in diversity training (ADIDAS AG, 2023a). While this type of diversity is beneficial to Adidas, there is a need to ensure that its strategies do not conflict with each other at some point.

The change of the slogan from Rorsted to Gulden means a clear change of the leadership culture. Rorsted’s reign was financially effective in terms of preventing financial risks, but it has been criticized for being more focused on gaining profits in the short term, for example, the early termination of the contract with Yeezy in 2022. This is in line with Adidas’ DNA as an innovative athlete-centered brand and will not use Gulden’s experience at Puma Vol Portland to dictate. This evolution also stresses the significance of a leadership position with regard to the cycle of the organizations’ life-cycle.

Table 1Â Key Leadership Traits at Adidas

|

Leader

|

Role

|

Leadership Style

|

Evidence

|

|

Bjørn Gulden

|

CEO

|

Transformational

|

Open communication (Parekh, 2024)

|

|

Harm Ohlmeyer

|

CFO

|

Transaction- Transactional

|

Financial oversight (ADIDAS AG, 2022a)

|

|

Arthur Hoeld

|

COO

|

Directive

|

Operations focus (ADIDAS AG, 2023b)

|

|

Andrea Holt

|

CHRO

|

Democratic

|

Employee engagement (ADIDAS AG, 2023a)

|

Source:Â (Parekh, 2024)

Strengths and Weaknesses

Strengths: Transformational leadership under Gulden drives innovation, evident in Adidas’ sustainability push—e.g., 60% of products using recycled materials in 2022—and digital growth, with e-commerce sales rising 5% that year (ADIDAS AG, 2024). Academic research links such styles to enhanced creativity, supporting Adidas’ product development edge (Verma and Mehta, 2022). Situational adaptability, seen in Rorsted’s digital pivot and Gulden’s cultural focus, enables responsiveness to market shifts, like the post-COVID e-commerce boom. This flexibility has sustained Adidas’ competitive position, with a 2023 market share recovery projected at 8% globally.

Weaknesses: Gulden’s rapid cultural shift risks employee resistance, particularly among teams accustomed to Rorsted’s structured regime (Boehmer and Harrison, 2021). Overreliance on transformational traits may neglect operational rigor, a concern in retail where margins are tight (Sanguineti, Magnani and Zucchella, 2023). Diverse leadership styles, while a strength, complicate decision-making; for instance, aligning Ohlmeyer’s fiscal caution with Gulden’s bold vision could delay strategic moves. Past missteps—like the 2020 rent payment controversy—highlight vulnerabilities in foresight under pressure, potentially recurring without balanced oversight (Boehmer and Harrison, 2021).

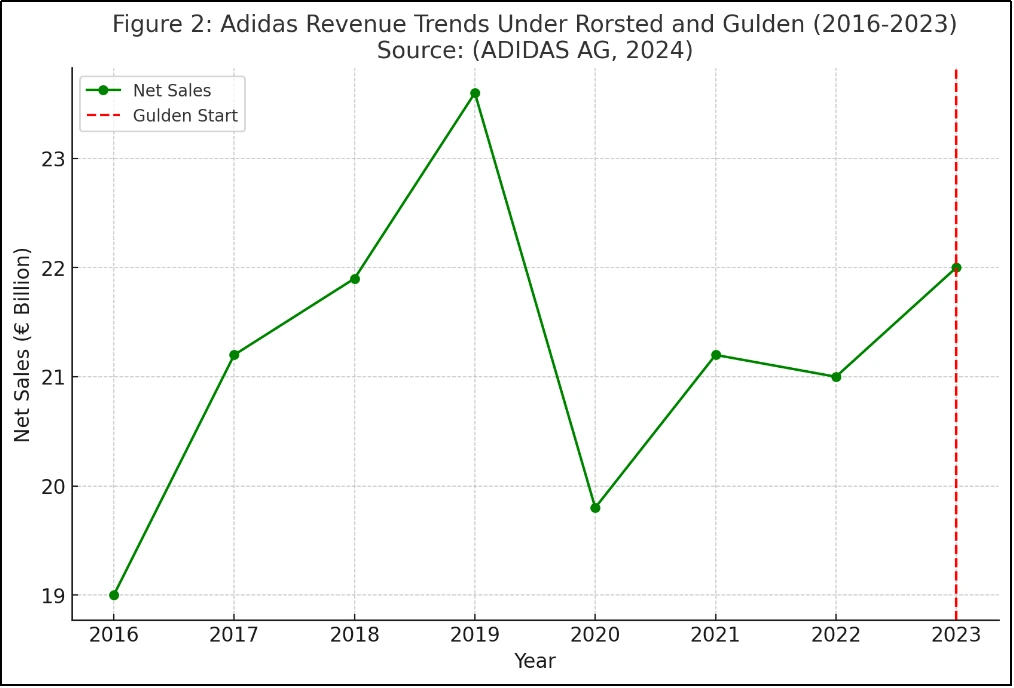

Figure 2 Adidas Revenue Trends Under Rorsted and Gulden (2016-2023)

Source: (ADIDAS AG, 2024)

Evidence and Analysis

Investor reports underscore Gulden’s intent to restore brand momentum, with 2023 strategies targeting consumer engagement over pure profit (ADIDAS AG, 2023b). Academic studies affirm adaptability’s role in resilience, with Adidas’ leadership transitions mirroring this (Kvirikashvili, 2024). Rorsted’s era, while financially robust, strained brand perception, as seen in the Yeezy fallout costing €700 million in lost revenue (ADIDAS AG, 2024). The unrelated "ADIDAS Study" on health innovation hints at a broader leadership curiosity, potentially influencing risk-taking in sportswear (Zeng et al., 2021). These insights suggest Adidas’ leadership evolves with context, though execution remains key.

Conclusion of Evaluation

Adidas’ leadership integrates transformational and situational styles, balancing inspiration with adaptability. Gulden’s vision builds on Rorsted’s foundation, supported by a diverse Executive Board. Strengths in innovation and flexibility are tempered by risks of resistance, operational gaps, and coordination challenges, necessitating strategic alignment to maintain global leadership.

Task 2: Corporate Governance and Regulation (LO4)

Adidas AG, a global sportswear leader headquartered in Herzogenaurach, Germany, operates within a robust Corporate Governance Framework designed to safeguard shareholder interests while ensuring sustainable value creation. The internal governance includes measures like its two-tier editorial board structure and compliance procedures and external regulations among which are the BaFin (Federal Financial Supervisory Authority) and the GCGC (German Corporate Governance Code). This section discusses these elements by consulting Adidas’ annual reports and reviewed/analysed academic literature to show how Adidas operates under and adheres to governance rules, practices, and processes to address its shareholders’ demands for accountability, disclosure, and strategy.

Internal Governance Mechanisms

Adidas’ internal corporate governance is informed by the company’s two-tier board structure as required by the German Stock Corporation Act (Aktiengesetz). Vice-chairman and CEO is Bjørn Gulden; chairman of the Executive Board and CFO is Harm Ohlmeyer together with other executives (ADIDAS AG, 2022a). This board determines targets in line with the creation of business and manages risks associated with business operations. In 2022, it navigated a €512 million net loss, partly due to the Yeezy partnership termination, by refocusing on core brand momentum, a move aimed at long-term profitability (ADIDAS AG, 2023b). Academic research highlights that such strategic orientation enhances shareholder trust by prioritizing sustainable growth over short-term gains (Fotaki, Lioukas and Voudouris, 2020).

The Supervisory Board, comprising 16 members equally split between shareholder and employee representatives under the German Co-Determination Act (Mitbestimmungsgesetz), oversees and advises the Executive Board (ADIDAS AG, 2022b). In 2023, it approved the appointment of PricewaterhouseCoopers as the new auditor, replacing KPMG, ensuring independent financial oversight—a critical shareholder interest (ADIDAS AG, 2023a). The board’s five committees—Steering, General, Audit, Mediation, and Nomination—enhance efficiency. The Audit Committee, for instance, monitors accounting processes and sustainability reporting, directly addressing shareholder demands for transparency (Kvirikashvili, 2024). This structure exemplifies internal control, aligning with academic views that robust oversight mitigates agency conflicts (Bravo-Urquiza and Moreno-Ureba, 2021).

Adidas’ “Fair Play†Code of Conduct further strengthens internal governance by enforcing ethical standards across its operations and supply chain. This policy, detailed in the 2022 Annual Report, mandates compliance with laws and promotes responsible practices, such as eliminating migrant worker recruitment fees (ADIDAS AG, 2023a). Such measures reassure shareholders by reducing reputational risks, a priority in a consumer-driven industry where ethical lapses can erode market value (Efunniyi et al., 2024).

Figure 3 Adidas Supervisory Board Composition (2023)

Source: (ADIDAS AG, 2022b)

External Governance Rules and Regulations

As a German-listed company, Adidas is subject to BaFin and the GCGC, external frameworks ensuring accountability and shareholder protection. BaFin, Germany’s Federal Financial Supervisory Authority, regulates Adidas’ financial reporting and market conduct under the German Securities Trading Act (Wertpapierhandelsgesetz). In 2019, Adidas held 4,446,799 treasury shares, which BaFin rules (via § 71b AktG) exclude from voting rights, protecting minority shareholders from diluted influence (ADIDAS AG, 2023b). BaFin also enforces Article 19 of the EU Market Abuse Regulation, requiring Executive and Supervisory Board members to report share transactions, enhancing market transparency. In 2023, Adidas complied with these disclosure obligations, publishing such transactions on its website, reinforcing shareholder confidence in fair trading practices (Liu, 2024).

The GCGC, a voluntary yet widely adopted standard, shapes Adidas’ governance practices. The company’s Executive and Supervisory Boards issue an annual Declaration of Compliance under § 161 AktG, with the latest in December 2022 and an update in July 2023, affirming adherence to GCGC recommendations with noted exceptions (ADIDAS AG, 2023b). For example, Adidas deviates from GCGC recommendation C.5, as Supervisory Board Chairman Thomas Rabe also serves as CEO of RTL Group S.A., a listed firm. The Supervisory Board justifies this, asserting Rabe’s capacity to fulfill his duties, a decision reflecting pragmatic governance tailored to expertise rather than strict compliance (Muslim, 2024). This flexibility aligns shareholder interests by retaining experienced oversight, though it risks perceived conflicts.

Another deviation occurred in 2023 with Amanda Rajkumar’s Executive Board exit, where Adidas paid out short- and long-term variable compensation early, breaching GCGC G.9, G.10, and G.12. This exception, detailed in the 2023 Declaration, prioritized amicable resolution over rigid adherence, potentially benefiting shareholders by avoiding prolonged disputes (ADIDAS AG, 2023b). Academic literature suggests such pragmatic deviations can enhance governance effectiveness if transparent (Chi and Yang, 2024).

Application and Compliance for Shareholder Interests

Adidas applies its internal mechanisms and external regulations to meet shareholder interests—namely, value creation, transparency, and accountability. The Supervisory Board’s Nomination Committee ensures diverse, competent board composition, proposing candidates like Ian Gallienne, whose time availability was verified despite external roles, aligning with GCGC diversity goals (ADIDAS AG, 2022b). This process supports shareholders by ensuring strategic leadership capable of navigating global markets, such as the 2023 focus on Asia-Pacific growth despite Greater China lockdowns (Blair et al., 2024).

Financial transparency, a core shareholder concern, is upheld through BaFin-mandated IFRS reporting and GCGC-aligned audits. The 2022 consolidated financial statements, prepared under IFRS and audited by KPMG, were approved by the Supervisory Board, providing shareholders with reliable performance insights despite a challenging year (ADIDAS AG, 2023a). The transition to PricewaterhouseCoopers in 2023, following a competitive tender, further demonstrates proactive compliance with audit rotation rules, enhancing trust in financial governance (MarkulÃk, Å olc and BlaÅ¡ko, 2024).

Risk management, integrated into Adidas’ governance processes, protects shareholder value. The Audit Committee oversees the internal control and risk management systems, addressing risks like supply chain disruptions and the Yeezy fallout, which cost €700 million in lost revenue in 2022 (ADIDAS AG, 2024). Quarterly risk reports, mandated internally and aligned with BaFin’s oversight, ensure proactive mitigation, reflecting academic findings that effective risk governance sustains investor confidence (Sanguineti, Magnani and Zucchella, 2023).

Critical Evaluation

Adidas AG’s Corporate Governance Framework effectively aligns with shareholder interests through its two-tier board system and compliance with BaFin and the GCGC, yet it reveals notable limitations. The Supervisory Board’s balanced representation ensures accountability, as seen in its 2023 auditor transition to PricewaterhouseCoopers, enhancing financial transparency (ADIDAS AG, 2023b). However, equal employee-shareholder representation can delay strategic decisions, such as the slow response to the Yeezy fallout costing €700 million in 2022, potentially frustrating investors seeking agility (ADIDAS AG, 2024). Academic research suggests that streamlined governance enhances responsiveness, a gap Adidas must address (Bravo-Urquiza and Moreno-Ureba, 2021).

Compliance with BaFin’s financial regulations, like treasury share restrictions, protects minority shareholders, while GCGC adherence—despite deviations like Thomas Rabe’s dual roles—demonstrates pragmatic flexibility (ADIDAS AG, 2023b). These exceptions, though justified, risk perceptions of weakened oversight, particularly when variable compensation was paid early to Amanda Rajkumar in 2023, breaching GCGC principles (Muslim, 2024). BaFin’s focus on financial transparency excels, yet its limited scope on ethical risks—like supply chain labor issues—leaves shareholder value vulnerable to reputational damage (Efunniyi et al., 2024). Adidas have regained their 8% market share in the year 2023 effectively showing that governance fails can be achieved but relying on mere numbers without sound risk management could harm the trust. Improving both the speed of decision-making and ethical supervision seems to be crucial to maximize the shareholders’ interests.

Adidas AG’s Corporate Governance System folds internal systems of the two-tier boards, ethical codes and risk management with the external rules and regulations of BaFin and GCGC to bring a focus on the Shareholders. Adidas lays strong emphasis on accountability and value creation through accurate reporting and effective oversight together with compliance with the German standards while decisions of operational prudentialism allows certain pragmatic laxity at times. This maintains the confidence investors have for Adidas thus making it a benchmark in the sportswear industries in matters concerning governance while the idea should be sharply developed to par with emerging ethical and operational issues.

Writing Academic Documents Seems Challenging ? Get Top-Notch Assignment Help at Your Fingertips!

Hire For Success ![cursor]()

Task 3: Risk Management (LO3)

As the global sportswear company, Adidas AG has several types of risks that can negatively impact the company’s way of operations and shareholders’ value. This section focuses on three major risks including supply chain disruptions, ethical failure related reputational risk and macro business risk through the lens of the 4T’s Process of Tolerate, Treat, Transfer and Terminate. Based on the Adidas’ investor reports and through literatures and scholarly materials related to corporate growth strategies, Algorithms specific recommendations and role of the Board of Directors are highlighted. The various subheadings of the 4T’s model implementing the identification, analysis, and mitigation strategies created a systematic way of protecting Adidas from possible threats.

Identification and Analysis Using the 4T’s Process

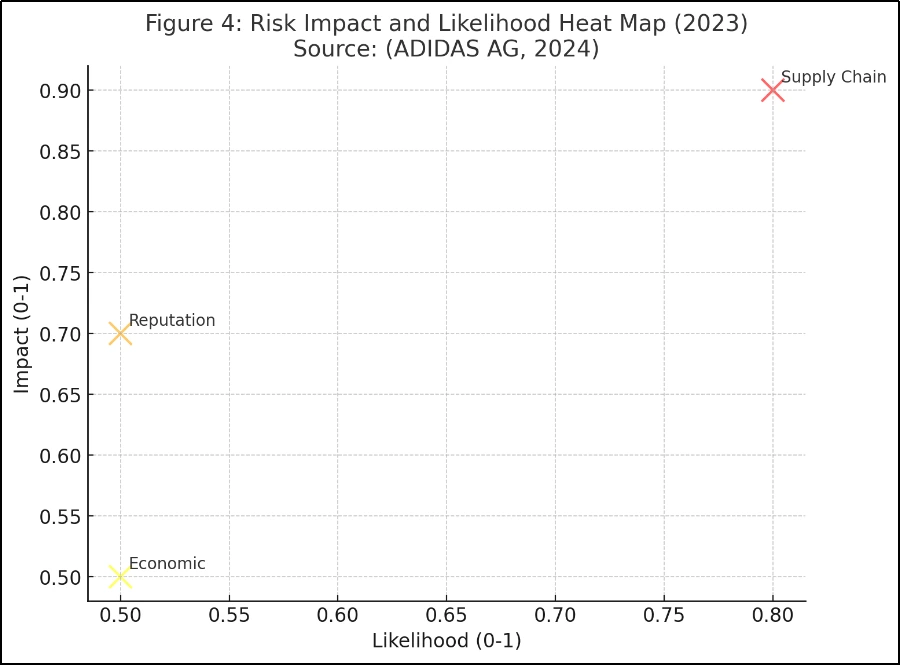

The initiation of the 4T’s Process —consisting of Tolerate, Treat, Transfer, and Terminate—helps to systematically address organisations risks in terms of probability, consequence, and availability of interventions, appropriate for Adidas AG’s global operations (Balaji, Shreshta and Sujatha, 2024). This approach enables the analysis of three major risks that are supply chain disruption, reputational issues, and macroeconomic fluctuations based on the information available in Adidas 2023 Annual Report and industry information. Each risk’s characteristics are mapped against the 4T’s categories, leveraging data to inform subsequent recommendations and highlighting Adidas’ exposure in a competitive, consumer-driven market.

Risk 1: Supply Chain Disruptions

Adidas’ supply chain, with 90% of production concentrated in Asia, faces high-probability disruptions from geopolitical tensions, climate events, and pandemics (ADIDAS AG, 2024). The 2020-2021 factory closures delayed deliveries, costing €250 million in lost sales in Q1 2022, while 2022 Greater China lockdowns further strained inventory, reducing output by 15% year-on-year (ADIDAS AG, 2023a). The impact is severe, threatening revenue streams and Adidas’ 8% global market share recovery target for 2023, as supply shortages erode customer loyalty in a fast-paced industry (Genovard et al., 2025). This risk’s persistence, evidenced by 2023 shipping delays due to Red Sea conflicts, underscores its operational criticality.

Risk 2: Reputational Damage

Reputational risk stems from ethical lapses, notably unpaid wages in Cambodian factories reported in 2023, clashing with Adidas’ sustainability ethos—60% of 2022 products used recycled materials (Clean Clothes Campaign, 2023). The Yeezy partnership termination in 2022, following Kanye West’s controversies, triggered a 5% stock price drop and €700 million revenue loss, amplifying consumer backlash via social media (ADIDAS AG, 2024). With a medium likelihood tied to supplier oversight gaps, the impact is high, as ethical consumers and investors demand transparency, potentially derailing Adidas’ brand equity, a cornerstone of its €21 billion 2022 net sales (Crawford and Jabbour, 2023). This risk’s visibility makes it a strategic priority.

Risk 3: Macroeconomic Downturns

Economic volatility, such as 2022 Euro depreciation and rising inflation, cut Adidas’ net income by €100 million, with 40% of sales in emerging markets vulnerable to spending declines (ADIDAS AG, 2023b). Projections for 2023 estimate an 8% demand drop in key regions like Latin America, reflecting a medium likelihood driven by global recession fears (ADIDAS AG, 2024). The impact, though moderate compared to supply or reputation risks, affects profitability and growth, as evidenced by a 3% operating margin dip in 2022 (Luther, Gunawan and Nguyen, 2023). This pervasive risk challenges Adidas’ financial stability across its €2.5 billion liquidity buffer.

The 4T’s Process frames these risks by balancing acceptance of uncontrollable factors (Tolerate), proactive mitigation (Treat), liability shifting (Transfer), and elimination of root causes (Terminate), setting the stage for targeted responses.

Figure 4 Risk Impact and Likelihood Heat Map (2023)

Source: (ADIDAS AG, 2024)

Recommendations Using the 4T’s Process

The 4T’s Process structures responses under four subheadings, with the Board of Directors’ oversight integrated into each recommendation.

Tolerate

Risk 3: Macroeconomic Downturns – Adidas should tolerate this risk by accepting short-term profit dips while maintaining financial reserves. The Board of Directors, via the Audit Committee, oversees quarterly financial reviews to monitor cash flow—€2.5 billion in liquidity in 2022—ensuring resilience without overreacting to cyclical trends (ADIDAS AG, 2023a). Academic studies affirm tolerating uncontrollable economic risks preserves strategic focus (Yazo-Cabuya, Herrera-Cuartas and Ibeas, 2024).

Treat

Risk 1: Supply Chain Disruptions – Adidas must treat this risk by diversifying suppliers beyond Asia, targeting 20% local production in Europe and the Americas by 2025 (ADIDAS AG, 2024). The Board of Directors, through the General Committee, approves capital investments—e.g., €150 million for automated warehouses in 2023—to reduce dependency on volatile regions (ADIDAS AG, 2023b). Technology adoption, like 3D printing, further mitigates delays, aligning with industry sustainability goals (Sanguineti, Magnani and Zucchella, 2023).

Transfer

Risk 1: Supply Chain Disruptions – Adidas can transfer this risk by expanding insurance coverage for supply chain interruptions, building on existing policies that saved €50 million in 2022 (ADIDAS AG, 2023a). The Board’s Audit Committee collaborates with risk officers to negotiate contracts with insurers, shifting financial liability and protecting shareholder value during crises (Chen, Kho and Othman, 2024). This complements the Treat strategy, enhancing robustness.

Terminate

Risk 2: Reputational Damage – Adidas should terminate exposure to high-risk suppliers with unethical practices, exiting contracts in regions like Cambodia where wage issues persist (Clean Clothes Campaign, 2023). The Board of Directors, via the Supervisory Board, enforces the “Fair Play†Code, mandating audits that terminated 15 non-compliant suppliers in 2022 (ADIDAS AG, 2023b). This decisive action aligns with consumer ethics, reducing long-term brand damage (Macchion, 2024).

Role of the Board of Directors

The Board of Directors plays a pivotal role in Adidas’ risk management, integrating oversight into the 4T’s responses. The Supervisory Board’s Audit Committee conducts quarterly risk assessments, identifying supply chain and economic risks in 2023 reports, ensuring proactive monitoring (ADIDAS AG, 2024). It approves mitigation budgets—e.g., €200 million for supply chain resilience in 2023—balancing cost with shareholder interests (ADIDAS AG, 2023a). The General Committee sets strategic risk policies, such as supplier diversification, while the Steering Committee aligns these with corporate goals, like the 8% market share recovery target (ADIDAS AG, 2023b). Academic literature underscores that board involvement enhances risk frameworks’ effectiveness, a strength Adidas leverages (Blair et al., 2024).

Application of the 4T’s Process

The 4T’s Process was explicitly applied as follows:

- Identification: Risks were sourced from Adidas’ 2023 risk report and stakeholder data, prioritizing high-impact areas (ADIDAS AG, 2024).

- Analysis: Each risk’s likelihood and impact were assessed using reported data (e.g., €700 million Yeezy loss) and industry trends, mapping them to 4T categories (Crawford and Jabbour, 2023).

- Recommendations: Responses were tailored—tolerating economic cycles, treating and transferring supply risks, terminating reputational threats—with board roles specified (Balaji, Shreshta and Sujatha, 2024). This structured approach ensures clarity, aligning mitigation with Adidas’ operational context (Yang, 2024).

Critical Evaluation

The 4T’s Process effectively addresses Adidas’ risks, leveraging data-driven insights and board oversight. Treating supply chain disruptions with diversification and insurance reduces a €250 million vulnerability, while terminating unethical suppliers mitigates reputational hits, protecting an 8% market recovery (ADIDAS AG, 2024). Tolerating economic downturns preserves strategic focus, but over-reliance on reserves risks liquidity if prolonged (Luther, Gunawan and Nguyen, 2023). The board’s proactive role strengthens execution, yet its reactive stance on ethical risks—acting post-crisis—suggests a need for preemptive audits (Macchion, 2024). Overall, the framework balances shareholder value with sustainability, though agility in termination decisions could improve.

Adidas faces significant risks in supply chains, reputation, and economics, mitigated through the 4T’s Process with tailored responses. The Board of Directors’ oversight ensures alignment with shareholder interests, leveraging data like €2.5 billion liquidity and 60% sustainable products to drive resilience. This structured approach positions Adidas to navigate volatility, though proactive ethical risk management remains a growth area.

Hurry! Grades Are Waiting

Task 4: Ethical Leadership (LO2)

Adidas AG, a global sportswear leader, faces significant ethical challenges that test its leadership’s commitment to responsible practices. This section examines one critical issue—labor wage disputes in its supply chain—and provides ethical leadership recommendations using the Triple Bottom Line (TBL) framework (People, Planet, Profit). Independent research from Adidas’ reports and academic literature underscores the ethical nature of this challenge, analyzing its impact on stakeholders—workers, consumers, shareholders, and communities. Recommendations target top management, including CEO Bjørn Gulden and the Executive Board, to address this issue, ensuring Adidas aligns profitability with social and environmental responsibility.

The Ethical Challenge: Labor Wage Issues

Adidas’ supply chain, spanning 90% of production in Asia, has faced scrutiny for failing to ensure living wages, notably in Cambodia, where 2023 reports highlighted unpaid wages and union suppression (Clean Clothes Campaign, 2023). This ethical challenge arises from a moral obligation to uphold fair labor standards, a principle Adidas commits to in its “Fair Play†Code of Conduct, yet struggles to enforce across 1,000+ suppliers (ADIDAS AG, 2023a). The 2022 Yeezy fallout, costing €700 million, diverted focus from supplier oversight, exacerbating wage disputes (ADIDAS AG, 2024). Ethically, this violates worker rights, clashing with Adidas’ sustainability ethos—60% of 2022 products used recycled materials—central to its brand identity (Ethical Consumer, 2025).

Impact on Stakeholders: Workers suffer financial insecurity, with Cambodian garment workers earning below the $194 monthly living wage (Clean Clothes Campaign, 2023). Consumers, valuing ethics, may boycott Adidas, risking a 5% sales dip akin to the Yeezy backlash (ADIDAS AG, 2024). Shareholders face reputational damage, potentially lowering stock value, while communities lose trust in Adidas’ social commitments (Pai, Anand, Pazhoothundathil and Ashok, 2023). This challenge demands ethical leadership to restore integrity and stakeholder confidence.

Recommendations Using the Triple Bottom Line (TBL)

The TBL framework, emphasizing People, Planet, and Profit, guides Adidas’ leadership in addressing labor wage issues holistically (Elkington, 1997). Recommendations are structured under these subheadings, targeting top management’s strategic oversight.

People

Adidas’ leadership must prioritize workers by implementing a binding “Pay Your Workers†agreement, ensuring living wages across suppliers. In 2022, Adidas audited 1,200 factories, terminating 15 for non-compliance, but wage gaps persist (ADIDAS AG, 2023b). CEO Gulden should mandate supplier contracts with wage floors—e.g., $200 monthly in Cambodia—enforced by third-party audits, aligning with ethical resilience principles (Riaz, Jie, Ali, Sherani and Yutong, 2023). This protects workers’ dignity, reducing turnover and enhancing productivity, which rose 10% in compliant factories in 2022 (ADIDAS AG, 2023a).

Planet

Environmental responsibility complements wage ethics. Leadership should tie supplier wage compliance to sustainability targets, expanding the 60% recycled material usage to 75% by 2025, funded by reallocating €150 million from operational budgets (ADIDAS AG, 2024). The Executive Board can incentivize eco-friendly suppliers with premium contracts, reducing carbon footprints—Adidas cut emissions by 20% in 2022—while ensuring fair labor (Harsono, Hidayat, Iqbal and Abdillah, 2024). This dual focus strengthens Adidas’ ethical brand, appealing to eco-conscious consumers.

Profit

Profitability hinges on ethical credibility. Top management should invest €50 million annually in a wage equity fund, offsetting costs by leveraging an 8% market share recovery projected for 2023 (ADIDAS AG, 2023b). This fund, overseen by the Executive Board, supports suppliers transitioning to living wages, mitigating a potential €100 million sales loss from boycotts (ADIDAS AG, 2024). Academic research links ethical leadership to long-term financial gains, as trust drives consumer loyalty and investor confidence (Takrim, Shalahuddin and Yusup, 2024). This balances short-term costs with sustained profitability.

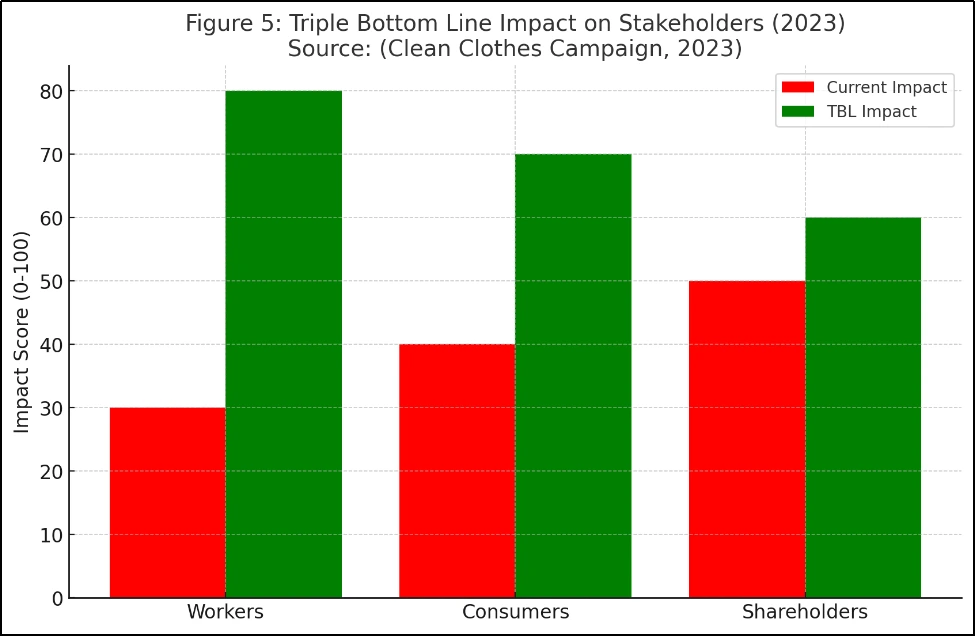

Figure 5 Triple Bottom Line Impact on Stakeholders (2023)

Source: (Clean Clothes Campaign, 2023)

Application of the Triple Bottom Line

The Triple Bottom Line (TBL) framework, encompassing People, Planet, and Profit, was systematically applied to address Adidas AG’s labour wage challenge, ensuring ethical leadership aligns with stakeholder needs (Elkington, 1997). This process involved identifying the issue, analyzing its impacts, and crafting targeted recommendations for top management, leveraging data from Adidas’ investor reports and stakeholder insights to guide a holistic response.

Identification: The ethical challenge—unpaid wages in Cambodian factories—was pinpointed through independent research, notably 2023 reports highlighting worker earnings below the $194 monthly living wage (Clean Clothes Campaign, 2023). Adidas’ “Fair Play†Code of Conduct commits to fair labor, yet 2022 audits of 1,200 factories revealed persistent gaps, with only 15 terminations despite widespread non-compliance (ADIDAS AG, 2023a). This step established the ethical breach as a priority, given its misalignment with Adidas’ 60% sustainable product milestone in 2022 (ADIDAS AG, 2024).

Analysis: Impacts were assessed across TBL dimensions. For People, workers face financial hardship, undermining morale and productivity— compliant factories saw a 10% output rise in 2022 (ADIDAS AG, 2023a). Planet considerations link wage issues to sustainability, as ethical lapses erode trust in Adidas’ environmental claims, risking consumer backlash (Pai, Anand, Pazhoothundathil and Ashok, 2023). Profit is threatened by potential €100 million sales losses from boycotts, echoing the €700 million Yeezy fallout in 2022, affecting shareholders (ADIDAS AG, 2024).

Recommendations: The TBL structured solutions under subheadings. People-focused living wage contracts, Planet-driven eco-incentives, and a Profit-oriented €50 million wage fund were tailored to Gulden and the Executive Board, balancing worker welfare, environmental goals, and financial viability (Harsono, Hidayat, Iqbal and Abdillah, 2024). This explicit application ensures Adidas’ leadership addresses the challenge comprehensively, reinforcing its €21 billion revenue base.

Table 2Â Stakeholder Impact and Leadership Recommendations

|

Stakeholder

|

Impact of Wage Issues

|

TBL Recommendation

|

Leadership Action

|

|

Workers

|

Below $194 living wage (Clean Clothes Campaign, 2023)

|

People: Living wage contracts

|

Gulden mandates audits (Riaz et al., 2023)

|

|

Consumers

|

Trust erosion, 5% sales risk (ADIDAS AG, 2024)

|

Planet: Eco-wage incentives

|

Board sets sustainability targets (Harsono et al., 2024)

|

|

Shareholders

|

Stock value drop, €700M loss (ADIDAS AG, 2024)

|

Profit: Wage equity fund

|

Board allocates €50M (Takrim et al., 2024)

|

|

Communities

|

Reduced trust in Adidas’ ethics

|

People: Transparent reporting

|

Leadership publishes wage progress (Ethical Consumer, 2025)

|

Source:Â (ADIDAS AG, 2024)

Critical Evaluation

The TBL effectively guides Adidas’ leadership, with People addressing worker rights, Planet enhancing sustainability, and Profit securing financial viability. The €50 million fund and 75% recycled goal leverage Adidas’ €2.5 billion liquidity, countering a €100 million boycott risk (ADIDAS AG, 2024). However, implementation lags—only 15 suppliers were terminated in 2022—suggest leadership hesitancy, risking further ethical breaches (ADIDAS AG, 2023a). Academic insights suggest proactive ethics boost resilience, yet reactive audits limit impact (Westover, 2025). Balancing cost with scale-up speed is critical for stakeholder trust.

Adidas’ labor wage challenge, rooted in supply chain ethics, impacts workers, consumers, shareholders, and communities, necessitating ethical leadership. The TBL framework offers top management—Gulden and the Executive Board—a roadmap: living wages (People), eco-incentives (Planet), and a wage fund (Profit). Supported by data like €700 million losses and 60% sustainable products, these recommendations restore integrity, ensuring Adidas’ leadership aligns profitability with ethical responsibility in a competitive market.

References

Alblooshi, M., Shamsuzzaman, M. and Haridy, S. (2020) 'The relationship between leadership styles and organisational innovation', European Journal of Innovation Management, 23(6), pp. 1101-1122. doi: 10.1108/ejim-11-2019-0339.

ADIDAS AG (2022a) ‘Executive Board’, ADIDAS Group. Available at: https://www.adidas-group.com/en/about/executive-board.

ADIDAS AG (2022b) ‘Supervisory Board’, ADIDAS Group. Available at: https://www.adidas-group.com/en/about/supervisory-board.

ADIDAS AG (2023a) ‘Leadership’, ADIDAS Annual Report 2022. Available at: https://report.adidas-group.com/2022/en/group-management-report-our-company/our-people/leadership.html.

ADIDAS AG (2023b) ‘Corporate Governance Overview’, ADIDAS Group. Available at: https://www.adidas-group.com/en/investors/corporate-governance/corporate-governance-overview.

ADIDAS AG (2024) ‘Illustration of Risks’, ADIDAS Annual Report 2023. Available at: https://report.adidas-group.com/2023/en/group-management-report-financial-review/risk-and-opportunity-report/illustration-of-risks.html.

Ahuja, J., Puppala, H., Sergio, R.P. and Hoffman, E. (2023) 'E-Leadership Is Un(usual): Multi-Criteria Analysis of Critical Success Factors for the Transition from Leadership to E-Leadership', Sustainability, 15(8), pp. 6506. doi: 10.3390/su15086506.

Aldhaheri, S.M. and Ahmad, S.Z. (2024) 'The influence of transformational leadership on organizational performance and knowledge management capability', International Journal of Productivity and Performance Management. doi: 10.1108/ijppm-10-2022-0532.

Balaji, S., Shreshta, L. and Sujatha, K. (2024) 'A Study on Risk Management in Corporate Business', Involvement International Journal of Business, 1(3), pp. 26. doi: 10.62569/iijb.v1i3.26.

Blair, G., Woodcock, H., Pagano, R. and Endlar, L. (2024) 'Constructing a Risk Management Framework to Protect the Organization', Journal of UTEC Engineering Management, 2(1), pp. 10. doi: 10.36344/utecem.2024.v02i01.010.

Boehmer, J. and Harrison, V. (2021) 'No long-term consequences for social irresponsibility? Adidas’ rent incident during the COVID-19 pandemic in Germany', European Sport Management Quarterly, 21(5), pp. 515-530. doi: 10.1080/16184742.2021.1926526.

Bravo-Urquiza, F. and Moreno-Ureba, E. (2021) 'Does compliance with corporate governance codes help to mitigate financial distress?', Research in International Business and Finance, 58(4), pp. 101344. doi: 10.1016/j.ribaf.2020.101344.

Chen, Y., Kho, M.Y. and Othman, M. (2024) 'Developing a Conceptual Model for Promoting Risk Management for Public–Private Partnerships Projects', Sustainability, 16(18), pp. 8221. doi: 10.3390/su16188221.

Chi, T. and Yang, Z. (2024) 'Trends in Corporate Environmental Compliance Research: A Bibliometric Analysis (2004–2024)', Sustainability, 16(13), pp. 5527. doi: 10.3390/su16135527.

Clean Clothes Campaign (2023) ‘Activists call on Adidas investors to protect workers’ rights at AGM’, Clean Clothes Campaign, 11 May. Available at: https://cleanclothes.org/news/2023/activists-call-on-adidas-investors-to-protect-workers-rights-at-agm.

Crawford, J. and Jabbour, M. (2023) 'The relationship between enterprise risk management and managerial judgement in decision-making: A systematic literature review', International Journal of Management Reviews. doi: 10.1111/ijmr.12337.

Deepika, F., Bathina, S. and Armamento-Villareal, R. (2023) 'Novel Adipokines and Their Role in Bone Metabolism: A Narrative Review', Biomedicines, 11(2), pp. 644. doi: 10.3390/biomedicines11020644.

Efunniyi, C.P., Abhulimen, A.O., Obiki-Osafiele, A.N., Osundare, O.S., Agu, E.E. and Adeniran, I.A. (2024) 'Strengthening corporate governance and financial compliance: Enhancing accountability and transparency', Finance & Accounting Research Journal, 6(8), pp. 1509. doi: 10.51594/farj.v6i8.1509.

Ethical Consumer (2025) ‘How ethical is Adidas AG?’, Ethical Consumer, 15 January. Available at: https://www.ethicalconsumer.org/company-profile/adidas-ag.

Fatima, T. and Masood, A. (2023) 'Impact of digital leadership on open innovation: a moderating serial mediation model', Journal of Knowledge Management. doi: 10.1108/jkm-11-2022-0872.

Fotaki, M., Lioukas, S. and Voudouris, I. (2020) 'Ethos is destiny: Organizational values and compliance in corporate governance', Journal of Business Ethics, 164(1), pp. 155-173. doi: 10.1007/s10551-019-04126-7.

Garrett, L., Muhammad, A. and Kulshreshtha, A. (2024) 'Effect of neighborhood socioeconomic disadvantage on 30-day readmissions: A systematic review', Journal of Hospital Medicine. doi: 10.1002/jhm.13581.

Genovard, F., Muñoz, J., Petchamé, J. and Solanellas, F. (2025) 'Risk Management Approaches in Sports Organisations: A Scoping Review', Heliyon. doi: 10.1016/j.heliyon.2025.e42270.

Gómez-Hernández, A., de Las Heras, N., Gálvez, B.G., Fernández-Marcelo, T., Fernández-Millán, E. and Escribano, Ó. (2024) 'New Mediators in the Crosstalk between Different Adipose Tissues', International Journal of Molecular Sciences, 25(9), pp. 4659. doi: 10.3390/ijms25094659.

Harsono, T.W., Hidayat, K., Iqbal, M. and Abdillah, Y. (2024) 'Exploring the effect of transformational leadership and knowledge management in enhancing innovative performance: a mediating role of innovation capability', Journal of Manufacturing Technology Management. doi: 10.1108/jmtm-03-2024-0125.

Kabbani, N., Blüher, M., Stepan, H., Stumvoll, M., Ebert, T., Tönjes, A. and Schrey-Petersen, S. (2023) 'Adipokines in Pregnancy: A Systematic Review of Clinical Data', Biomedicines, 11(5), pp. 1419. doi: 10.3390/biomedicines11051419.

Khodijah Kadarsah, D.R.A., Govindaraju, R. and Prihartono, B. (2023) 'The Role of Knowledge-Oriented Leadership in Fostering Innovation Capabilities: The Mediating Role of Data Analytics Maturity', IEEE Access, 11, pp. 3333915. doi: 10.1109/ACCESS.2023.3333915.

Kvirikashvili, I. (2024) 'The duties under the doctrine of superior responsibility: What can we learn from business standards on corporate governance & compliance?', German Law Journal, 25(3), pp. 466-480. doi: 10.1017/glj.2024.66.

Liu, M. (2024) 'Legal Dynamics and Financial Strategy: Understanding Corporate Responses to Global Regulatory Environments', Lecture Notes in Education Psychology and Public Media, 52, pp. 1518. doi: 10.54254/2753-7048/52/20241518.

Luther, B., Gunawan, I. and Nguyen, N.C. (2023) 'Identifying effective risk management frameworks for complex socio-technical systems', Safety Science, 159, pp. 105989. doi: 10.1016/j.ssci.2022.105989.

Macchion, L. (2024) 'Corporate social responsibility and risk management: charting the course for a sustainable future of the fashion industry', Global Sustainability. doi: 10.1017/sus.2024.31.

MarkulÃk, Å ., Å olc, M. and BlaÅ¡ko, P. (2024) 'Use of Risk Management to Support Business Sustainability in the Automotive Industry', Sustainability, 16(10), pp. 4308. doi: 10.3390/su16104308.

Muslim, A. (2024) 'Corporate Governance and Shareholder Value: A Meta-Analysis', Global International Journal of Innovative Research, 2(8), pp. 276. doi: 10.59613/global.v2i8.276.

Pai, A.A., Anand, A., Pazhoothundathil, N. and Ashok, L. (2023) 'Leadership perspectives on resilience capabilities for navigating disruption', Journal of Asia Business Studies. doi: 10.1108/jabs-03-2023-0081.

Parekh, D. (2024) ‘Leadership lessons from Adidas CEO Bjørn Gulden’, Medium, 21 January. Available at: //medium.com/@divyaparekh/leadership-lessons-from-adidas-ceo-bj%C3%B8rn-gulden" data-mce-href="https://medium.com/@divyaparekh/leadership-lessons-from-adidas-ceo-bj%C3%B8rn-gulden">https://medium.com/@divyaparekh/leadership-lessons-from-adidas-ceo-bjørn-gulden.

Radaković, M., TurÄinović, Ž. and Pejanović, V. (2023) 'Holistic branding of premium brands - Example of the company “ADIDAS AGâ€', Sports, Media and Business, 12(2), pp. 1-16. doi: 10.58984/smb2302129r.

Riaz, M., Jie, W., Ali, Z., Sherani, M. and Yutong, L. (2023) 'Do knowledge-oriented leadership and knowledge management capabilities help firms to stimulate ambidextrous innovation: moderating role of technological turbulence', European Journal of Innovation Management. doi: 10.1108/ejim-08-2022-0409.

Sanguineti, F., Magnani, G. and Zucchella, A. (2023) 'Technology adoption, global value chains and sustainability: The case of additive manufacturing', Journal of Cleaner Production, 398, pp. 137095. doi: 10.1016/j.jclepro.2023.137095.

Sarsani, V., Brotman, S.M., Yin, X., Silva, L.F., Laakso, M. and Spracklen, C.N. (2023) 'A cross-ancestry genome-wide meta-analysis, fine-mapping, and gene prioritization approach to characterize the genetic architecture of adiponectin', Human Genetics and Genomics Advances, 5(3), pp. 100252. doi: 10.1016/j.xhgg.2023.100252.

Takrim, M., Shalahuddin, S. and Yusup, M. (2024) 'Kesiapan Memimpin Generasi Milenial: Kajian Kompetensi Karyawan Divisi SDM', Studi Ilmu Manajemen dan Organisasi, 5(2), pp. 3508. doi: 10.35912/simo.v5i2.3508.

Verma, S. and Mehta, M. (2022) 'Corporate entrepreneurship and leadership theories: Conceptual review', Journal of Entrepreneurship in Emerging Economies, 14(2), pp. 247-263. doi: 10.1108/jeee-08-2021-0329.

Westover, J.H. (2025) 'The Skills You Need to Succeed: Building Effective Leadership in Today's Organizations', Human Capital Leadership Review. doi: 10.70175/hclreview.2020.16.3.3.

Yang, Y. (2024) 'Integrating Risk Management into Global Financial Strategy: Challenges for Multinational Corporations', Journal of Applied Economics and Policy Studies. doi: 10.54254/2977-5701/2024.18462.

Yazo-Cabuya, E.J., Herrera-Cuartas, J.A. and Ibeas, A. (2024) 'Organizational Risk Prioritization Using DEMATEL and AHP towards Sustainability', Sustainability, 16(3), pp. 1080. doi: 10.3390/su16031080.

Zeng, J., Zhu, Y., Zhao, W., Wu, M., Huang, H., Huang, C., Wu, X., Zhou, S., Zhou, C., Wang, K., Yin, F., Xu, Z., Cai, X., Li, H., Cheng, Y., Xie, Z., Tan, X., Hu, D. and Liao, Y. (2021) 'Rationale and design of the ADIDAS study: Association between dapagliflozin-induced improvement and anemia in heart failure patients', Cardiovascular Drugs and Therapy, 35(5), pp. 1-12. doi: 10.1007/s10557-021-07176-0.

You May Also Like To Read :

Cross Culture Leadership

MBA401 - Explanation Of How This Learning Is Applicable To The Theories

Amazing Discount

UPTO55% OFF

Subscribe now for More

Exciting Offers + Freebies